A Cost Most Businesses Don’t Measure Properly

There is a hidden cost inside almost every international transaction.

It doesn’t show up clearly in invoices.

It’s rarely questioned internally.

And over time, it compounds into a significant financial drain.

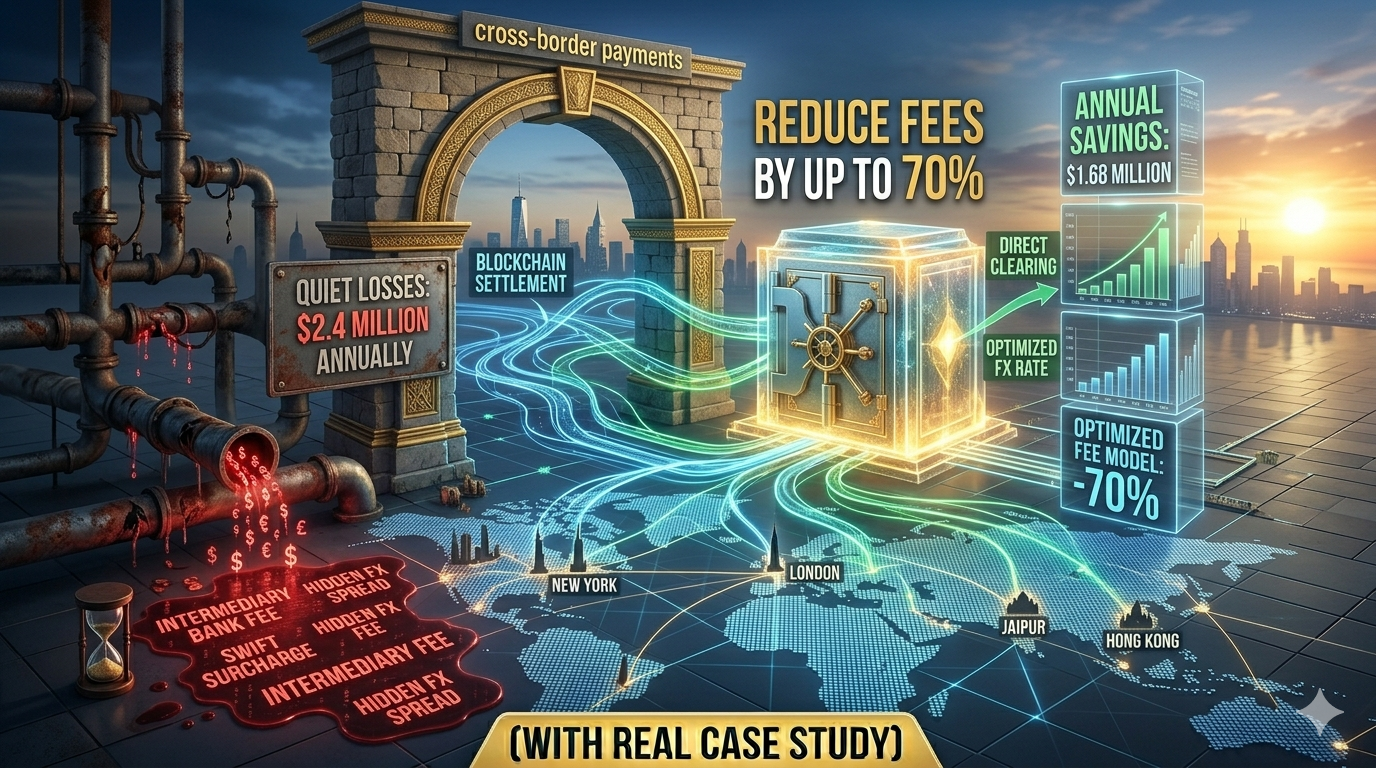

We’re talking about cross-border payment fees.

For most businesses, these costs are treated as “standard.”

But when you take a closer look — especially for transactions above $50,000 and scaling up to $10,000,000 — the numbers tell a different story.

What appears to be a routine transaction often includes:

Multiple layers of fees

Invisible exchange rate markups

Operational inefficiencies

And collectively, they can erode 5% to 10% of every payment.

At scale, that’s not a cost.

That’s a structural inefficiency.

The $1,000,000 Question

Let’s take a simple scenario.

A business sends $1,000,000 to an international supplier.

On paper, it looks straightforward.

But in reality:

A portion is deducted as transfer fees

Another portion disappears in intermediary handling

The largest chunk is often lost in foreign exchange margins

By the time the payment settles, the actual cost may exceed $50,000.

Now multiply that across:

Monthly supplier payments

Vendor settlements

Cross-border operations

Suddenly, the business isn’t just paying for transactions.

It’s funding inefficiency.

Why This Problem Still Exists

The natural question is:

Why hasn’t this been solved already?

The answer lies in how global payment systems were built.

Traditional cross-border infrastructure is not a single system — it’s a network of systems stitched together over decades.

Each layer was designed for:

Control

Compliance

Local banking ecosystems

Not for:

Speed

Cost efficiency

Global scalability

So what we see today is a system where:

Payments move through multiple institutions

Each institution adds cost

Each step introduces delay

This model worked in a slower, less connected world.

But in today’s environment, it creates friction.

The Hidden Layer: Foreign Exchange Margins

Most businesses focus on transfer fees.

But the real cost often lies elsewhere.

Foreign exchange (FX) margins

Banks don’t usually convert currency at the market rate.

They apply a spread — often small in percentage terms, but large in absolute value.

For example:

A 2% margin on a $1,000,000 transaction = $20,000

A 3% margin = $30,000

This is where the majority of cost leakage happens.

And because it’s not always transparent, it often goes unnoticed.

Why High-Value Transactions Are More Affected

Smaller payments absorb inefficiencies.

Large payments amplify them.

For transactions between:

$50,000 and $10,000,000

Even minor inefficiencies translate into:

Significant financial loss

Reduced margins

Slower capital movement

This directly impacts:

Cash flow planning

Supplier negotiations

Business scalability

In other words, payment inefficiency becomes a strategic issue.

Rethinking the Problem

Instead of asking:

“How do we reduce fees slightly?”

The better question is:

“Why are we paying these fees at all?”

Because once you ask that, the conversation shifts from optimization to transformation.

A Structural Shift: From Banking Rails to Digital Infrastructure

Over the past few years, a new approach has emerged.

Instead of relying on traditional banking rails, businesses are exploring:

Digital payment infrastructure powered by stable-value assets

This model changes the fundamentals of how payments move.

Instead of:

Passing through multiple intermediaries

Waiting for batch processing

Incurring layered fees

Payments become:

Direct

Faster

More cost-efficient

What Actually Changes in This Model

The difference is not incremental.

It’s structural.

1. Fewer Intermediaries

Transactions are executed more directly, reducing:

Handling layers

Associated costs

2. Faster Settlement

Instead of waiting days, payments settle within minutes.

This improves:

Liquidity

Operational efficiency

3. Reduced Cost Leakage

Without multiple intermediaries and FX spreads:

Total cost drops significantly

4. Predictable Value

Using USD-linked digital instruments eliminates:

Currency volatility

Unexpected losses

The 70% Cost Reduction — What It Actually Means

When businesses say they reduce costs by up to 70%, it doesn’t come from a single change.

It comes from eliminating multiple layers of inefficiency:

Reduced intermediary fees

Lower conversion costs

Faster processing (less operational delay)

So instead of losing:

$50,000–$100,000 per $1M transaction

Businesses retain a much larger portion of their capital.

A New Layer of Value: Beyond Just Payments

One of the more interesting developments in this space is the introduction of:

Digital payment-linked tokens

In some models, businesses receive a digital asset alongside each transaction.

This creates an additional layer of value:

The asset can be held

Traded

Utilized within broader ecosystems

This shifts payments from being purely transactional…

…to becoming value-generating.

Where This Shift Matters Most

While this transformation is global, its impact is especially strong in regions where traditional systems are less efficient.

Africa

In markets such as:

Nigeria

Kenya

South Africa

Businesses often face:

Higher transaction costs

Limited banking infrastructure

Reducing payment friction here has immediate impact.

Latin America

In countries like:

Brazil

Mexico

The challenge is often:

Currency volatility

Complex financial systems

A more stable, predictable payment layer changes the equation.

Strategic Implications for Businesses

At a surface level, this looks like a finance optimization.

But at a deeper level, it affects strategy.

Businesses that reduce payment inefficiencies can:

Improve margins

Move capital faster

Scale operations more efficiently

In competitive markets, this becomes a real advantage.

A Shift in Mindset

For years, businesses have accepted payment costs as fixed.

But that assumption is now outdated.

The real shift is not just in technology — it’s in mindset:

From “managing costs”

To “eliminating inefficiencies”

Questions Businesses Should Start Asking

Instead of:

“What are our transaction fees?”

Start asking:

How many intermediaries are involved?

What is our true FX cost?

How long does capital remain locked?

What is the opportunity cost of delays?

These questions lead to better decisions.

The Bigger Picture

Payments are no longer just operational.

They are becoming:

A financial optimization lever

A strategic growth enabler

A competitive differentiator

Businesses that recognize this early will have an edge.

Conclusion

Cross-border payment fees have been accepted for too long as unavoidable.

But when examined closely, they reveal:

Structural inefficiencies

Hidden cost layers

Opportunities for transformation

The shift toward modern payment infrastructure is not just about saving money.

It’s about building a more efficient, scalable business.