When businesses evaluate cross-border payment solutions, the conversation usually starts with a simple question:

“What is the best way to send and receive international payments?”

For years, the default answer has been:

Bank transfers

SWIFT network

Traditional payment processors

But today, a new option is rapidly gaining attention:

Stablecoin-based payment systems

This is no longer a theoretical discussion. Businesses across industries are actively comparing:

Stablecoin payments vs traditional banking systems

Speed vs reliability

Cost vs efficiency

Innovation vs legacy infrastructure

In this guide, we’ll break down this comparison in a clear, data-driven, and real-world context, including a practical case study to help you understand which approach is better for modern cross-border business payments — especially for high-value transactions between $50,000 and $10,000,000.

Understanding the Two Systems

Before comparing, let’s define both approaches clearly.

Traditional Payment Systems

These include:

Bank wire transfers

SWIFT network

Correspondent banking

How it works:

Payment is initiated from the sender’s bank

Routed through intermediary banks

Processed and settled at the recipient’s bank

Stablecoin Payment Systems

These use digital currencies such as:

USDT

USDC

How it works:

Payment is initiated through a digital platform

Transferred directly using blockchain infrastructure

Received almost instantly

Case Study: A Real Business Scenario

Let’s consider a realistic example.

Scenario:

A company based in Europe needs to pay a supplier in Nigeria:

Transaction Amount: $500,000

Option 1: Traditional Banking System

Process:

Payment initiated via bank

Routed through 2–3 intermediary banks

Converted into local currency

Outcome:

Time taken: 3–5 business days

Total fees: ~$20,000–$35,000

FX loss: Additional $10,000–$15,000

Total cost: ~$30,000–$50,000

Option 2: Stablecoin Payment System

Process:

Payment initiated via platform

Transferred using stablecoins

Received directly

Outcome:

Time taken: Minutes

Fees: Significantly lower

FX loss: None

Total cost: Reduced by up to 70%

Key Insight:

The difference is not marginal — it is transformational.

Cost Comparison Breakdown

Let’s take a closer look at costs for different transaction sizes:

Amount

Traditional Cost (5–10%)

Stablecoin Cost

$50,000

$2,500–$5,000

Much lower

$500,000

$25,000–$50,000

Significantly reduced

$1,000,000

$50,000–$100,000

Up to 70% savings

Over time, these savings compound into massive financial advantages.

Speed Comparison: Why It Matters

In global business, speed is not just convenience — it’s a competitive advantage.

Traditional System

Dependent on banking hours

Delays due to intermediaries

Time zone issues

Stablecoin System

24/7 transactions

Near-instant settlement

No dependency on banks

Faster payments = better cash flow + faster business cycles

Risk Comparison

Traditional Payments

FX volatility

Payment delays

Transaction failures

Stablecoin Payments

Stable value (USD-linked)

Transparent transactions

Reduced operational risk

Where Each System Still Works

To be fair, both systems have their place.

Traditional Payments Are Still Used For:

Legacy systems

Domestic banking

Regulatory-heavy environments

Stablecoins Are Ideal For:

Cross-border payments

High-value transactions

Global operations

Emerging markets

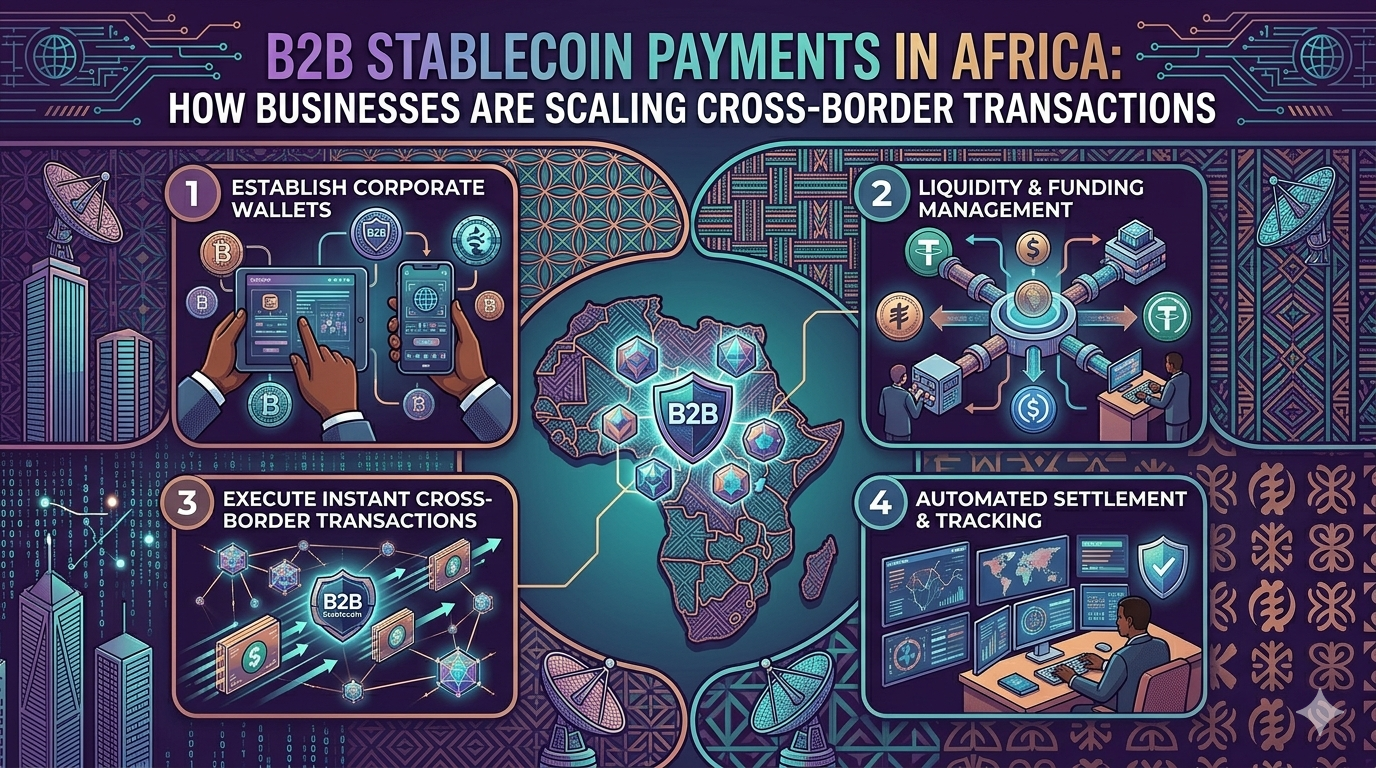

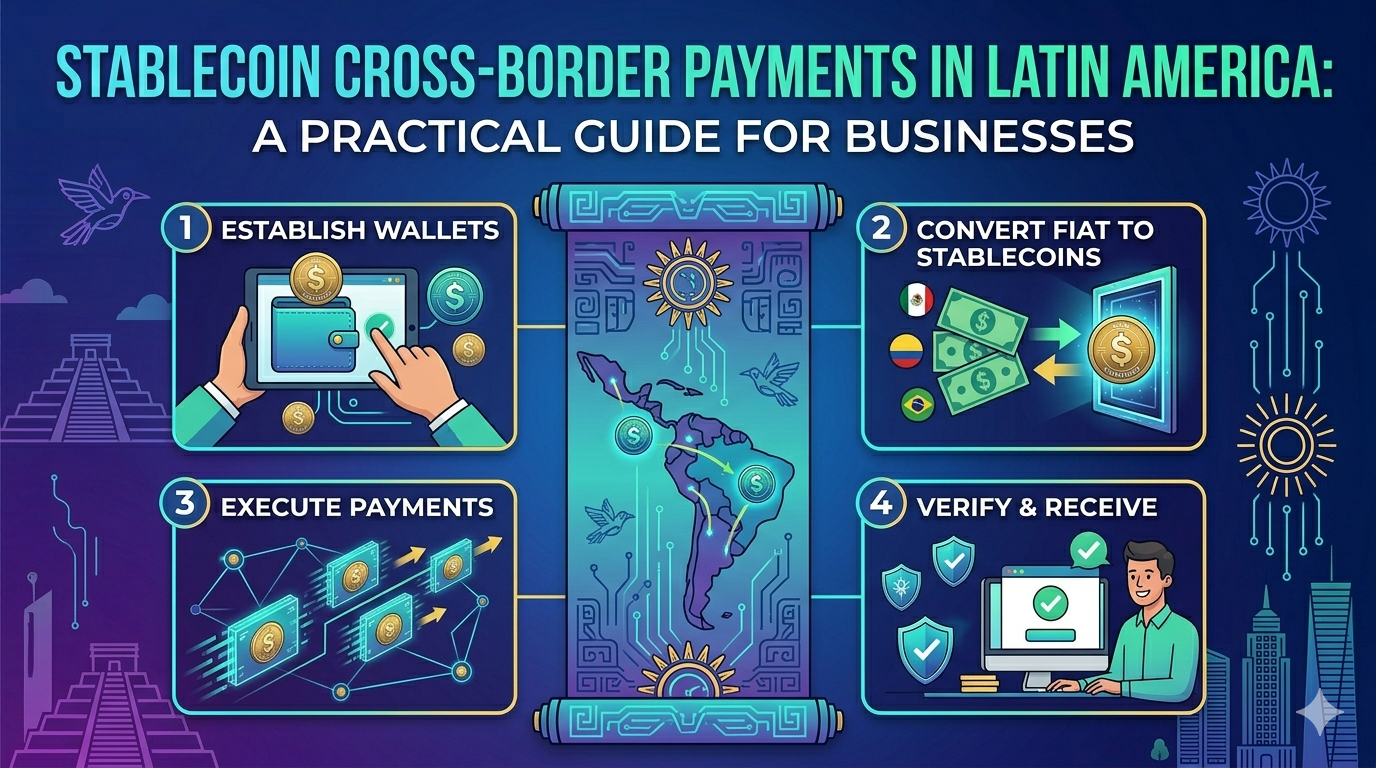

Africa & Latin America: Where the Difference is Huge

Africa

Countries like:

Nigeria

Kenya

South Africa

Face:

High transaction fees

Limited banking infrastructure

Stablecoins provide a much better alternative.

Latin America

Countries like:

Brazil

Mexico

Face:

Currency volatility

Payment inefficiencies

Stablecoins solve both issues.

Unique Advantage: Value Beyond Payments

One of the most interesting developments is:

Free digital payment token (eSgC) with every transaction

This creates:

Additional financial value

Tradable digital asset

Extra benefit beyond payments

This is something traditional systems cannot offer.

Enterprise Perspective: What Decision Makers Should Consider

When evaluating payment systems, enterprises should look at:

Total Cost (Not Just Visible Fees)

Hidden costs often matter more than visible ones.

Speed & Efficiency

Faster payments improve operations.

Scalability

Can the system handle high-value transactions?

Global Reach

Does it work across multiple regions?

The Final Verdict

When comparing stablecoin vs traditional payment systems:

Traditional systems are reliable but inefficient

Stablecoin systems are faster, cheaper, and more scalable

Strategic Insight

This is not just a technology shift.

It’s a shift in how businesses think about payments.

From cost center → to strategic advantage

Frequently Asked Questions

Which is better for cross-border payments?

Stablecoin-based systems offer better speed, cost efficiency, and transparency.

Can stablecoins handle large transactions?

Yes, they are ideal for payments between $50K and $10M.

Are stablecoin payments secure?

Yes, when using reliable and compliant platforms.

Why are businesses switching?

To reduce costs, improve speed, and scale globally.

Conclusion

Cross-border payments are evolving.

Businesses now have a clear choice:

Continue with traditional systems

Or adopt more efficient, modern infrastructure