Introduction: Africa’s Payment Problem — and the Opportunity

Africa is one of the fastest-growing regions for cross-border trade, digital services, and global business expansion. From fintech startups in Lagos to export companies in Nairobi and enterprise firms in Johannesburg, businesses across the continent are increasingly operating beyond borders.

Yet one major challenge continues to slow this growth:

👉 Cross-border payments in Africa are still expensive, slow, and inefficient.

For businesses handling transactions between $50,000 and $10,000,000, these inefficiencies are not minor inconveniences — they directly affect:

Profit margins

Cash flow

Supplier relationships

Global scalability

This is why a growing number of companies are adopting a new approach:

👉 B2B stablecoin payments in Africa

This shift is not just technological — it’s strategic.

The Reality of B2B Payments in Africa Today

To understand the transformation, we first need to look at the current state of payments across the continent.

1. Fragmented Financial Systems

Africa is not a single unified financial market.

Each country has:

Different banking systems

Different regulations

Different currencies

👉 This fragmentation makes cross-border payments complex and inefficient.

2. High Transaction Costs

Businesses sending international payments often face:

Bank fees

Intermediary charges

FX conversion margins

👉 Total costs can reach 5%–10% per transaction

3. Currency Volatility

Currencies in many African markets fluctuate significantly.

This creates:

Unpredictable payment values

Financial risk

Reduced profitability

4. Slow Settlement Times

Traditional cross-border payments typically take:

👉 2–5 business days (or more)

For businesses, this leads to:

Delayed operations

Slower supply chains

Cash flow issues

5. Limited Transparency

Tracking payments across multiple banks is often difficult.

Businesses frequently lack clarity on:

Where the payment is

When it will arrive

What fees were deducted

Why This Matters for High-Value Transactions

For small payments, these inefficiencies may be manageable.

For large payments, they become critical.

Example:

A business sending $500,000 internationally:

Fees: $25,000–$50,000

FX losses: $10,000+

👉 Total potential loss: $35,000–$60,000

Multiply this across multiple transactions, and the impact becomes massive.

What Are B2B Stablecoin Payments?

B2B stablecoin payments refer to business-to-business transactions conducted using stable digital currencies.

Common examples include:

USDT (Tether)

USDC (USD Coin)

Key Characteristics:

Pegged to USD (stable value)

Blockchain-based transfers

Fast global settlement

👉 Unlike traditional systems, these payments do not rely on multiple intermediaries.

Why Stablecoin Payments Are Gaining Adoption in Africa

Businesses across Africa are increasingly adopting stablecoin-based payment systems — and for good reason.

1. Reduced Transaction Costs

By removing intermediaries, stablecoin payments significantly lower fees.

👉 Businesses can save up to 70% on payment costs

2. Faster Settlement

Transactions are completed within minutes, not days.

👉 This improves:

Cash flow

Business speed

Operational efficiency

3. No FX Losses

Stablecoins are USD-backed.

👉 This eliminates:

Currency conversion losses

Exchange rate volatility

4. Greater Accessibility

Businesses can operate globally without depending on:

Local banking limitations

Complex financial infrastructure

5. Full Transparency

Blockchain-based systems provide:

Real-time tracking

Clear transaction records

How Businesses Are Using Stablecoin Payments in Africa

Let’s look at real business use cases.

1. Supplier Payments

Companies paying international suppliers can:

Reduce delays

Lower costs

Improve relationships

2. Cross-Border Trade

Import/export businesses benefit from:

Faster settlements

Predictable payment values

3. Enterprise Transactions

Large organizations moving funds across countries can:

Simplify operations

Improve efficiency

4. Invoice Payments

High-value invoice settlements become:

Faster

More reliable

Cost-efficient

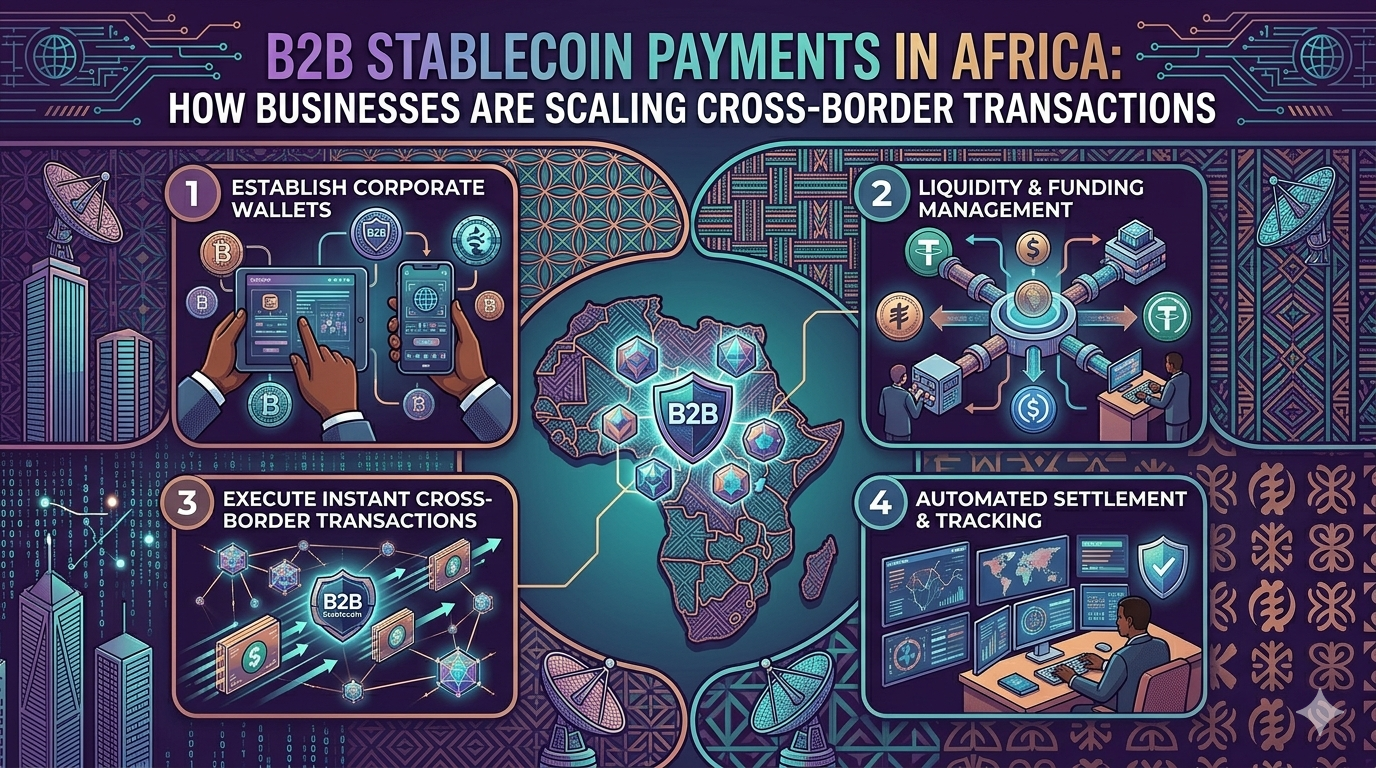

Step-by-Step: How B2B Stablecoin Payments Work

Step 1: Payment Initiation

Business enters payment details and invoice information.

Step 2: Funding the Transaction

Payment is funded using stablecoins such as USDT or USDC.

Step 3: Validation

System verifies transaction details.

Step 4: Settlement

Payment is completed within minutes.

👉 The entire process is faster and more efficient than traditional systems.

Key African Markets Leading Adoption

Nigeria

High demand for cross-border payments

FX restrictions driving alternative solutions

Kenya

Strong fintech ecosystem

Growing adoption of digital payments

South Africa

Advanced financial infrastructure

Increasing enterprise adoption

👉 These markets are leading the transition toward modern payment systems.

Strategic Benefits for Businesses

Adopting B2B stablecoin payments is not just about reducing costs.

It creates long-term strategic advantages.

Improved Profit Margins

Lower transaction costs directly increase profitability.

Faster Business Operations

Payments no longer slow down processes.

Better Financial Control

Real-time tracking improves decision-making.

Global Expansion

Businesses can scale internationally with fewer barriers.

Challenges and Considerations

While adoption is growing, businesses should consider:

Regulatory Environment

Regulations vary across countries.

👉 It’s important to use compliant platforms.

Integration

Businesses may need to adapt their existing systems.

Education

Teams must understand how the system works.

👉 With the right approach, these challenges are manageable.

The Future of Payments in Africa

Africa is not just catching up — it’s leapfrogging traditional systems.

Businesses are moving directly to:

Faster infrastructure

Digital payment systems

Cost-efficient models

👉 Stablecoin payments are at the center of this transformation.

Conclusion

B2B stablecoin payments in Africa are not just a trend — they are a response to real business challenges.

For companies handling high-value transactions, this approach offers:

Lower costs

Faster payments

Greater efficiency

Improved scalability

Final Thought

If your business operates across Africa…

👉 The real question is not whether stablecoin payments work

👉 It’s how much you could save by adopting them

Frequently Asked Questions

What are B2B stablecoin payments?

They are business-to-business transactions conducted using stable digital currencies like USDT and USDC.

Why are stablecoin payments growing in Africa?

Because they reduce costs, improve speed, and solve traditional banking limitations.

Can businesses send large payments using stablecoins?

Yes, they are ideal for transactions between $50K and $10M.

Are stablecoin payments secure?

Yes, when processed through reliable and compliant platforms.

How do stablecoins reduce payment costs?

By eliminating intermediaries and reducing FX-related losses.